Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Have you ever wondered, “Can debt collectors come after a company that’s dissolved?” It seems like a simple question, after all, if a business is officially closed, shouldn’t its debts just vanish? Unfortunately, the answer isn’t always that straightforward. The truth is, in some cases, creditors can still pursue obligations even after a company has been dissolved and knowing when and why this can happen is crucial for any former business owner.

When I first dissolved a small business years ago, I thought all my liabilities would disappear overnight. Spoiler alert, they didn’t! A couple of unexpected letters from collection agencies taught me a hard lesson about how company dissolution works and what obligations survive. Understanding these rules early can save you from surprise claims, legal headaches, and even personal financial exposure.

In this article, we’ll dive into the nitty-gritty of company dissolution and answer the burning question: can debt collectors come after a company that’s dissolved? We’ll cover the legal rules, common exceptions, and practical steps you can take to protect yourself. By the end, you’ll have a clear picture of what happens when a business closes and how to stay on solid ground financially.

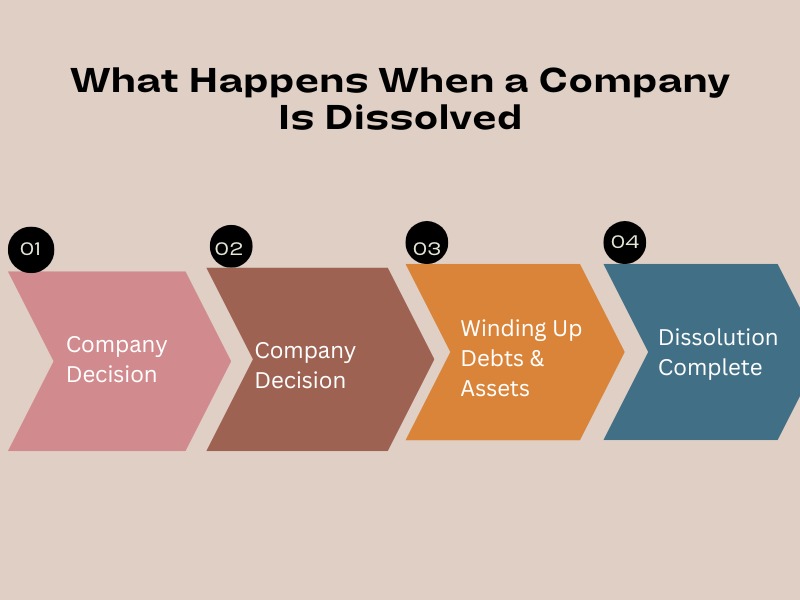

Dissolving a company isn’t just about closing the doors and calling it a day. When I went through it for the first time, I realized there’s a formal process, legal obligations, and several steps you can’t skip, especially if you want to avoid surprises later. Here’s what I learned.

When you dissolve a company, you’re essentially telling the government and the public that your business no longer exists. The formal process usually involves:

I remember thinking this would be quick, but even small mistakes in paperwork can delay the process and leave your company technically “active” in the eyes of creditors.

Not all dissolutions are the same.

Voluntary Dissolution

Involuntary Dissolution

I learned the hard way that involuntary dissolution can trigger unexpected communications from debt collectors. It’s one of the reasons why I always recommend getting professional guidance.

Even after deciding to dissolve a company, you’re still responsible for certain obligations:

Skipping any of these steps can lead to personal liability, depending on your role in the company. This is exactly where the question can debt collectors come after a company that’s dissolved? starts to matter.

“Winding up” is basically the cleanup phase. It involves:

Think of it as sorting through every corner of your business before shutting the doors for good. If debts aren’t properly addressed here, creditors may have legal grounds to pursue claims even after dissolution.

When I first dissolved my company, I believed all debts vanished. Not true! Some common misconceptions include:

The reality is that certain debts can survive the dissolution, and this is why it’s so important to understand the process fully.

When I first asked myself, “Can debt collectors come after a company that’s dissolved?” I assumed the answer would be a simple no. But after digging into the rules, I realized it’s more complicated than I expected. Even after a company officially closes, debt collectors can sometimes pursue claims, depending on the type of debt, legal protections, and the company’s structure.

The general rule is that once a company is dissolved, its legal existence ends. However, this doesn’t always mean debts disappear. Certain obligations, like taxes, employee wages, and debts backed by personal guarantees, can still be enforced. Debt collectors may have legal avenues to pursue these claims, especially if the winding-up process was incomplete.

Not all debts are treated the same:

Knowing the type of debt is key to understanding potential risks.

Laws vary, but statutory regulations often protect former business owners. For example:

These rules create a balance, some debts survive, while others simply vanish if not claimed in time.

I came across a few cases that really illustrate the point:

These stories made it clear that dissolution doesn’t automatically erase all liability.

Several factors influence whether debt collectors can pursue a dissolved company:

Understanding these factors is crucial to knowing your exposure and protecting yourself financially.

Even after you dissolve a company, there are specific situations where debt collectors can still come after you. I learned this the hard way when I thought closing my business meant all liabilities vanished—but certain exceptions can put former owners back in the spotlight.

One of the biggest surprises for me was realizing that personal guarantees can make you personally responsible for company debts. If you signed a guarantee for a loan, credit line, or lease, the creditor can pursue you even after the company is officially dissolved. Directors of a company can also be held liable if the company was mismanaged or if laws weren’t followed during its operation.

If a company was involved in fraud or serious mismanagement, debt collectors, or even regulatory authorities, can pursue claims after dissolution. I’ve seen cases where former owners were contacted years later because the court determined that financial obligations were evaded intentionally. It’s not common, but it’s a risk you can’t ignore.

Certain debts survive dissolution by law. Taxes owed to local, state, or federal authorities, along with unpaid employee wages, are not erased just because the business closed. Creditors in these categories often have legal priority, meaning they can pursue collections against remaining assets, or sometimes even against directors personally.

In some cases, creditors can apply to the court to revive a dissolved company to collect unpaid debts. I was surprised when I read about a case where a creditor successfully reopened a company to recover outstanding loans. This legal option exists in many jurisdictions, and it’s another reason why thorough record-keeping and proper winding up are critical.

While dissolution provides many protections, it doesn’t make all debts disappear. Personal guarantees, statutory obligations, and fraud-related claims are common exceptions. Understanding these scenarios helps you plan ahead, avoid surprises, and answer the crucial question: can debt collectors come after a company that’s dissolved?

Going through the dissolution process without a plan can be stressful, and I learned that the hard way. Even if you think all your debts are settled, a few small oversights can lead to unexpected claims. Here’s what I recommend to protect yourself when closing a business.

Before officially dissolving your company, make sure all outstanding debts are addressed. Paying creditors, suppliers, and service providers upfront can save you from potential legal headaches. I’ve seen cases where business owners thought minor invoices weren’t important, only to be contacted months later by debt collectors.

If you’ve signed any personal guarantees, check if they can be removed or settled. Personal guarantees are a common reason former business owners get pursued even after dissolution. I made it a point to review every loan and contract to avoid surprises, and it was worth the effort.

Keep a clear record of all communications with creditors, including emails, letters, and payment confirmations. When a debt collector tries to contact you after dissolution, having documented proof of settlements or agreements can save you a lot of stress.

Different states or countries have different rules for dissolved companies and debt recovery. I spent time reviewing local laws to know what creditors could legally pursue and what protections were in place. Knowing your rights and obligations in your jurisdiction is essential.

Finally, don’t hesitate to get professional guidance. A lawyer familiar with business dissolution can help you identify potential risks, ensure all obligations are properly handled, and reduce the chance of post-dissolution claims. It might feel like an extra expense, but it can save a lot more in the long run.

By taking these steps, you’re not only closing your company properly, you’re protecting yourself from unnecessary financial stress and answering the big question: can debt collectors come after a company that’s dissolved?

Even after properly dissolving a company, you might still hear from debt collectors. When I got my first post-dissolution notice, I was panicked but knowing how to handle these situations makes a huge difference.

Not every claim you receive is valid. Always ask for written proof of the debt, including amounts, dates, and the original creditor. I learned that some collectors try to pursue debts that were already settled or outside the legal recovery period. Verifying legitimacy protects you from unnecessary stress and potential scams.

Even if the debt seems questionable, respond promptly and professionally. I found that polite, documented communication often stops aggressive or harassing behavior. Keep emails or letters factual, stating your understanding of the debt and referencing any agreements or settlements from the dissolution process.

If a legitimate debt surfaces, consider negotiating a settlement or payment plan. Sometimes creditors are willing to accept a reduced amount, especially if the company no longer exists and assets are limited. Disputing incorrect claims is also possible, just make sure to keep everything in writing.

In some cases, it’s helpful to send a formal legal notice to debt collectors clarifying that the company has been dissolved and outlining any protections you have under the law. I did this once, and it immediately stopped further collection attempts.

Finally, keep all documents, communications, and payment confirmations organized. You never know when you might need to reference them for future legal or financial matters. Proper record-keeping is one of the most effective ways to protect yourself after dissolution.

Handling debt collectors calmly and systematically helps you avoid panic and ensures that your rights are protected, once again answering the question: can debt collectors come after a company that’s dissolved?

So, can debt collectors come after a company that’s dissolved? The short answer is: sometimes. Going through my own experience, I realized that while proper dissolution protects you in many ways, certain debts and obligations can survive the process. Understanding these nuances is key to avoiding surprises.

First, know the difference between secured and unsecured debts, and recognize which ones may still be collectible. Secured debts and statutory obligations, like taxes or employee wages, are often enforceable even after dissolution. Personal guarantees and mismanagement can also expose you to post-dissolution claims.

Second, don’t underestimate the importance of proper documentation and record-keeping. Every communication, payment, and agreement matters. When debt collectors come knocking, having your records organized makes all the difference.

Third, take proactive steps during dissolution. Settle debts where possible, review personal guarantees, and consult a legal professional. These actions can drastically reduce the chances of post-dissolution claims.

Finally, remember that every situation is unique. Corporate structure, jurisdiction, timing, and legal protections all play a role in determining whether debt collectors can pursue claims. By understanding your risks and acting responsibly, you can dissolve your company confidently and minimize surprises.

If you’ve gone through this process yourself, or are about to, take a moment to review your obligations carefully. Staying informed is your best defense. And if you have any stories, tips, or questions, don’t hesitate to share them in the comments, it helps everyone navigate this tricky area with less stress.

Check out our latest articles on Insurance.