Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Did you know that nearly 40% of self-storage renters purchase insurance they never actually use? It’s true, and a lot of people later wonder if they can cancel. If you’re asking, “Can I cancel Avid self-storage insurance premium now?” you’re not alone.

In this article, I’ll break down exactly what you need to know: how cancellation works, what fine print matters, when you might be eligible for a refund, and smart alternatives if you’re looking to save money. Whether you’ve just signed up or you’ve been paying for months, knowing your rights and options could save you serious cash!

When I first rented a storage unit, I remember thinking, “Why do I need insurance for stuff that’s just sitting in a locked space?” But then the manager explained how common accidents are, flooded basements, break-ins, even something as simple as a busted pipe leaking into units. That’s where Avid self-storage insurance comes in.

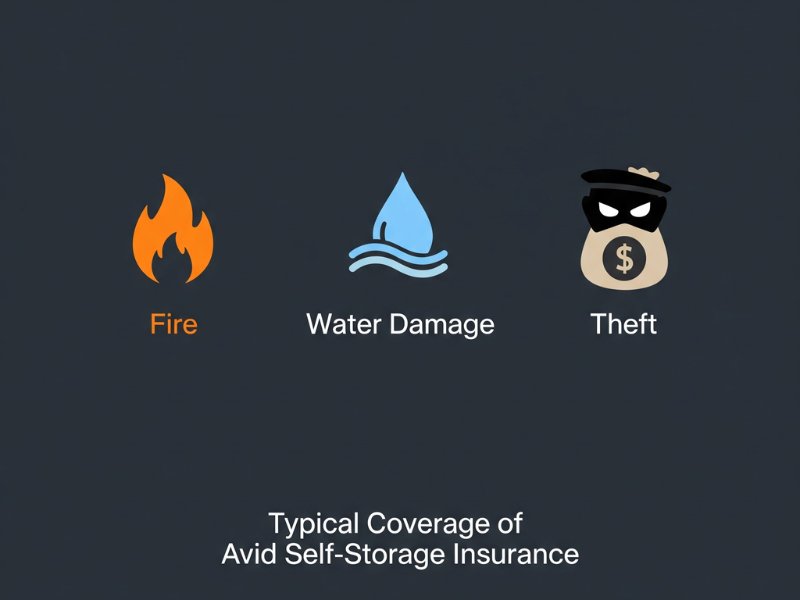

Avid self-storage insurance is basically a protection plan you buy on top of your storage rental. It covers your belongings if something unexpected happens, like fire, theft, or water damage. Think of it as a safety net for the “just in case” moments nobody plans for.

From what I’ve seen in most policies, coverage usually includes:

I once had a friend who discovered mold on her stored clothes. She assumed the insurance would cover it, but nope, it didn’t. That’s why reading the fine print matters more than you’d think.

Here’s a little secret: storage companies push insurance because it protects them as much as it protects you (SelfStorage.com on Insurance Requirements). If something happens to your unit, they don’t want to be responsible. By making insurance mandatory, they shift the risk onto you and the insurer.

Avid is one of the common providers these facilities partner with, which is why you’ll often see it bundled into the rental process. Sometimes you can’t even get a unit without either buying their insurance or showing proof of your own.

Most premiums run between $10–$20 a month depending on your coverage amount. The more valuables you store, the higher the coverage (and cost). It feels small month to month, but if you’re renting long-term, it adds up quickly. That’s usually when people start asking, “Can I cancel Avid self-storage insurance premium?”

If you’ve ever looked at your bill and thought, “Wait, why am I paying this extra $12 every month?” you’re definitely not alone. That question is exactly why this guide exists.

Short answer? Yes, you can cancel, but it’s not always as simple as clicking a button. When I first looked into cancelling mine, I assumed I could just stop paying and that would be the end of it. Big mistake. Instead, I got hit with a late notice because I hadn’t followed the proper steps.

Most of the time, Avid will let you cancel under certain conditions:

I once canceled after moving to a new apartment because my renter’s insurance extended to storage units. But the storage facility didn’t automatically remove Avid from my bill, I had to show them my new policy before they stopped charging me.

Here’s something a lot of people don’t know consumer protection laws in the U.S. generally give you the right to cancel insurance policies at any time (FTC on Insurance), as long as you follow the cancellation process. That doesn’t mean you’ll always get a refund, but it does mean you’re not trapped forever.

The tricky part is buried in the fine print. Some contracts require written notice, others need proof of alternate coverage, and a few even specify a minimum notice period. I’ve seen people get stuck paying an extra month simply because they didn’t give enough notice.

Whenever I sign something now, insurance, gym membership, even my cell phone contract, I go straight to the “cancellation” section of the agreement first. It’s boring, but trust me, it saves headaches later.

Here’s a warning: if you cancel without showing proof of other coverage, the storage company may not let you keep the unit. Many facilities require insurance as part of the rental agreement. So cancelling Avid without a backup plan could mean either losing your unit or being forced to take their in-house policy again.

That’s why, before you even think about cancelling, make sure you have your ducks in a row. Otherwise, you’ll find yourself paying twice, or worse, scrambling to keep your stuff safe.

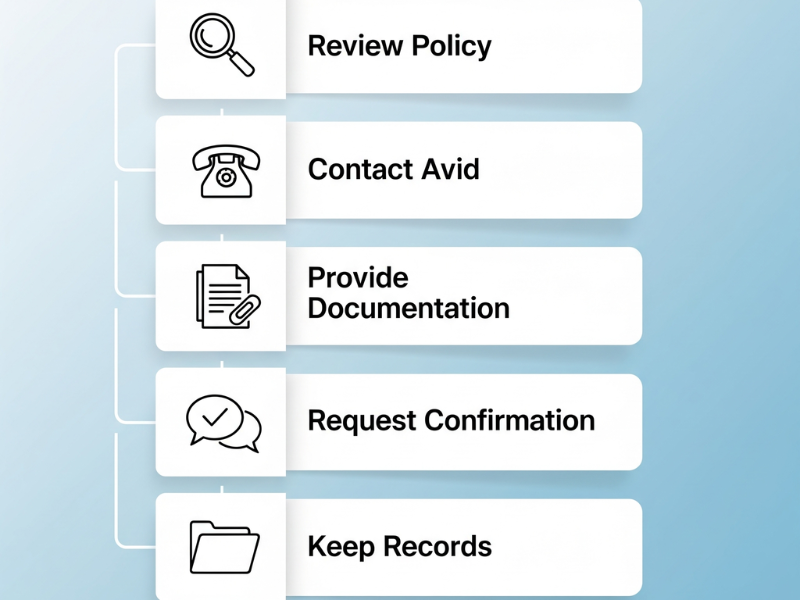

When I finally decided to cancel my Avid self-storage insurance, I thought it would be a quick email and done. Nope. It turned into a bit of back-and-forth with the storage office and Avid’s customer service. If you don’t want that hassle, here’s the process I wish I had followed from the start.

Before you do anything, pull up your policy documents. Look specifically for sections labeled “Termination,” “Cancellation,” or “Refunds.” I know, it feels tedious, but that’s where all the rules are hiding. For example, some Avid policies require written notice, while others accept an email or phone call.

I always highlight the cancellation section with a marker or screenshot it. That way, when I’m talking to a rep, I can quote their own policy back to them if there’s any pushback.

Here’s where most people get tripped up: some cancellations have to go through the storage facility, not Avid directly. In my case, the facility manager had the authority to remove the charge from my account once I showed alternate coverage.

This part is non-negotiable. If you’re cancelling because you switched to renters or homeowners insurance, you’ll need to show proof. That means sending a copy of your new declarations page or policy number.

When I forgot to send mine, the cancellation just sat in limbo. No one bothered to tell me until I noticed another charge on my bill the next month. Lesson learned.

If you’re cancelling because you emptied your unit, ask the facility to send Avid a “move-out confirmation.” That usually triggers an automatic cancellation.

Never assume a phone call is enough. Always, always ask for written proof that your Avid insurance has been cancelled. An email is fine, it just gives you something to point to if charges show up later.

I’ve made this mistake before tossing receipts or deleting emails too quickly. But when it comes to cancelling insurance, you’ll want to keep everything, emails, letters, call notes, for at least a few months. If a billing error happens down the line, you’ll have the paper trail ready.

When I finally got my Avid self-storage insurance cancelled, I immediately wondered, “Am I getting any money back?” The answer isn’t always straightforward, and I’ve seen plenty of people get frustrated here. Let me break it down for you.

Most Avid policies offer a pro-rated refund if you’ve already paid for the month but cancelled mid-cycle. For example, if you paid $15 for the month and cancelled halfway through, you might get around $7.50 back.

I learned this the hard way. I didn’t ask about the refund upfront, and they assumed I didn’t want it. Make sure to explicitly request a pro-rated refund, and you’ll avoid leaving money on the table.

Not all charges are refundable. Some policies may have an administrative or cancellation fee, usually $5–$10. I’ve seen people get hit with this even after paying for just a couple of weeks.

It’s small, but it adds up if you’re juggling multiple storage units or policies. Always check the fine print to see if any fees apply before you cancel.

Refunds aren’t instant. From my experience, it usually takes 2–6 weeks for the money to hit your account. Some banks process it faster, others take longer. Keep an eye on your statements to make sure the refund actually arrives.

Send your cancellation request via email instead of just calling. Email creates a paper trail, and in my case, the finance team processed it quicker once they had a written record.

There are cases where refunds aren’t given at all:

I remember one friend who tried to cancel two days after the monthly cycle ended. She assumed she’d get the next month back, but the policy deadline had already passed. Definitely a bummer, and an easy mistake to avoid if you check your dates.

When I first thought about cancelling my Avid self-storage insurance, I was all about cutting costs. But after doing a little digging, I realized there were smarter ways to save money without leaving my stuff completely unprotected.

If you already have renters or homeowners insurance, it might cover items in a storage unit unit (Insurance Information Institute). Before cancelling Avid, I called my insurance agent to confirm. Turns out, my policy covered up to $1,000 in stored belongings. By showing proof of this coverage to the storage facility, I was able to cancel Avid and still have my items protected.

This not only reduced my monthly expenses but also simplified my coverage. One policy, one premium, fewer headaches.

Not all policies are “one-size-fits-all.” Sometimes, simply reducing your coverage limits can bring down your premium significantly. For example, I realized most of my stored items weren’t valuable enough to justify the full $10,000 coverage I had initially selected. Dropping the limit cut my monthly payment nearly in half, without leaving me exposed to major losses.

Here’s something many people overlook: your storage facility might be willing to work with you. I once asked if they had a lower-cost plan for long-term renters, and they offered a basic coverage option for just a few dollars less than Avid. It’s not a massive discount, but it saved me a few bucks each month and kept me insured.

Sometimes, cancelling isn’t worth the risk. If you have high-value items, antiques, or electronics in storage, keeping Avid’s full coverage may make more sense than trying to save $10–$15 per month. I’ve seen friends regret cancelling only to deal with a small fire that destroyed a few items—trust me, it’s not worth the gamble.

Cancelling Avid self-storage insurance sounds simple, but trust me, there are plenty of ways it can go wrong. I’ve seen friends and even a few clients make these mistakes, and it usually costs them time, money, or both.

One of the biggest mistakes is assuming that cancelling automatically cancels your obligation to have coverage. Many storage facilities require proof that you’re covered elsewhere. I had a friend cancel without sending her renters insurance info, and she ended up paying another month’s premium before they accepted her proof.

Moving out of your storage unit does not always trigger automatic cancellation. I made this exact mistake once. I thought the facility would notify Avid, but I got charged for another month. Always double-check that your cancellation is officially processed.

Phone calls are great, but they aren’t official proof. I’ve had situations where verbal confirmation didn’t hold up, and I had to dig through emails to prove I’d cancelled. Always request an email or written notice from either the storage facility or Avid.

Some policies have specific deadlines for requesting refunds. Miss it, and you could lose out on money you’re entitled to. I once waited a week too long to request a pro-rated refund, and it wasn’t honored. Lesson learned: mark your calendar and act promptly.

It may sound boring, but reading your policy thoroughly saves a ton of headaches. Things like cancellation fees, notice periods, or coverage gaps are often buried in the small print. I’ve personally highlighted these sections in my contracts ever since; it’s a small step that prevents big mistakes.

By keeping these mistakes in mind and taking proactive steps, cancelling your Avid self-storage insurance can be much smoother, and you’ll avoid paying for coverage you no longer need.

At the end of the day, cancelling your Avid self-storage insurance premium isn’t just about cutting costs it’s about making smart choices for your belongings and your wallet. I’ve learned that taking a few minutes to read the fine print, check deadlines, and request written confirmation can save you from surprise charges and unnecessary stress.

If your stored items are valuable, sometimes keeping coverage is worth it for peace of mind. But if you’ve moved out, switched to a better policy, or just want to reduce expenses, following the proper steps means you can cancel confidently, and maybe even get a pro-rated refund along the way.

Think of it as a little strategy game: gather your documents, confirm your coverage, and communicate clearly with both Avid and your storage facility. Do it right, and you’ll not only avoid headaches but also take control of your storage costs.

So, take a moment today to review your policy, line up your alternatives, and make the move that works best for you. And if you’ve got tips, tricks, or stories about cancelling storage insurance, share them, someone else reading this might thank you for it!

Want to dive deeper into financial topics? Check out our other guides:

You can usually cancel at any time, but it depends on your policy terms. Some policies have monthly deadlines or require notice before the next billing cycle. I once assumed I could cancel mid-month without issue and ended up paying another month—so always check the dates first.

Potentially, yes. Many facilities require proof of insurance as part of the rental agreement. Cancelling Avid without alternate coverage could mean losing your unit or being forced to take another policy. Always confirm with the facility before cancelling.

Sometimes you can, but not always. I had a friend who moved to a different facility, thinking her Avid policy would automatically follow her. It didn’t. Policies are usually tied to a specific unit or facility, so check with Avid if you’re relocating.

Stopping payments without formally cancelling is risky. You might face late fees, collections, or a negative mark on your account. In my experience, always submit a formal cancellation request—never just stop paying.

Refunds typically take 2–6 weeks to appear, depending on the payment method and processing time. Sending cancellation requests via email usually speeds up the process because it creates a paper trail.