Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Replacing or upgrading an HVAC system can feel overwhelming, especially when you look at the price tag. Did you know the average cost of a new HVAC system in the U.S. runs between $5,000 and $12,000? That’s not pocket change! For many homeowners, the big question isn’t if they need a replacement, but how to pay for it. The good news? Financing options make it possible to install a new unit without draining your savings. In this guide, we’ll explore your options, what to expect with financing, and how to make the smartest decision for your budget. So, can you finance a new HVAC system? let’s find out.

When my old HVAC system went out one summer, I thought I could just tough it out with a few fans until I had enough saved. Big mistake. Within a week, my house felt like a sauna, and I caved. That’s when I learned the hard truth, HVAC systems aren’t cheap. Financing suddenly didn’t sound like a luxury; it sounded like survival.

The sticker shock of a new system can make anyone hesitate. Depending on the size of your home and the type of unit, you could be looking at $7,000–$12,000 or more. Paying that all at once feels impossible for most families. Financing spreads that cost into monthly payments, which makes it easier to budget. Instead of draining your savings or swiping a high-interest credit card, you can break the expense into smaller, predictable chunks. Think $150–$300 a month instead of $10,000 upfront.

Here’s the thing: HVAC systems don’t usually quit when it’s convenient. Mine gave out during peak summer heat, and I couldn’t wait months to save up. Financing allows you to move forward immediately. That means no sweating through July or freezing through January while you scramble for cash. It also helps avoid bigger repair bills from running an old system past its limit. Delaying replacement often costs more in the long run.

Another reason financing makes sense? Newer systems are far more energy-efficient. The one I financed cut my utility bill by almost 25% compared to my old clunker. That’s money back in your pocket every month, which helps offset the financing payment. Plus, an upgraded HVAC system makes your home more comfortable year-round and can even boost resale value if you’re planning to sell. Buyers love knowing they won’t have to deal with a failing unit right after moving in.

At the end of the day, financing isn’t just about affording the system, it’s about making a smart, timely investment in your home and comfort.

When I first started looking into HVAC financing, I was shocked at how many different routes there actually were. It’s not just “sign a loan and hope for the best.” Each option has its own perks, risks, and little quirks that can make or break your decision. Let’s walk through the most common ones you’ll find in 2025.

Some HVAC brands, think Carrier, Trane, Lennox, offer their own in-house financing. When I replaced my system, I was offered a 0% APR promo for 18 months through the manufacturer’s program. It felt a lot like buying a car: you get dealer-backed financing straight from the company making the product. The upside? Simple and often low interest if you qualify. The downside? Those deals sometimes vanish after the promo period, and rates can spike if you miss a payment.

If you’re working with a local HVAC contractor or a big-box retailer like Home Depot, chances are they’ll pitch you a financing plan. These can be convenient since you don’t need to find your own lender. The catch is that interest rates vary wildly. I’ve seen offers as low as 5% and as high as 22%. It’s worth comparing this with an outside lender because convenience can come at a cost.

Banks and online lenders will happily give you a personal loan to cover an HVAC replacement. I tried this route once and liked the predictability, fixed interest rate, fixed monthly payment, and no strings attached to a particular contractor. Approval depends heavily on your credit, though. If your score is strong, this can be one of the best middle-ground options. If not, interest rates can shoot into the double digits.

If you own your home and have equity, tapping into it for an HVAC system is a solid option. A home equity loan gives you a lump sum, while a HELOC acts more like a credit line you can draw from. I’ve seen people use these to cover big upgrades since the rates are often lower than personal loans. But and this is a big but, your house is collateral. Miss too many payments, and the lender could come knocking.

I’ll admit, I used a credit card for one smaller HVAC repair, but I’d think twice before putting a full system on one. The only time it makes sense is if you snag a 0% APR intro card and know you’ll pay it off before the promo ends. Otherwise, you’re looking at interest rates north of 20%, which is brutal. Credit cards should be the “last resort” unless you’ve got a tight repayment plan.

In short, the “best” financing option depends on your credit, budget, and how soon you need that system up and running. Each path has trade-offs, but knowing them ahead of time keeps you from getting blindsided.

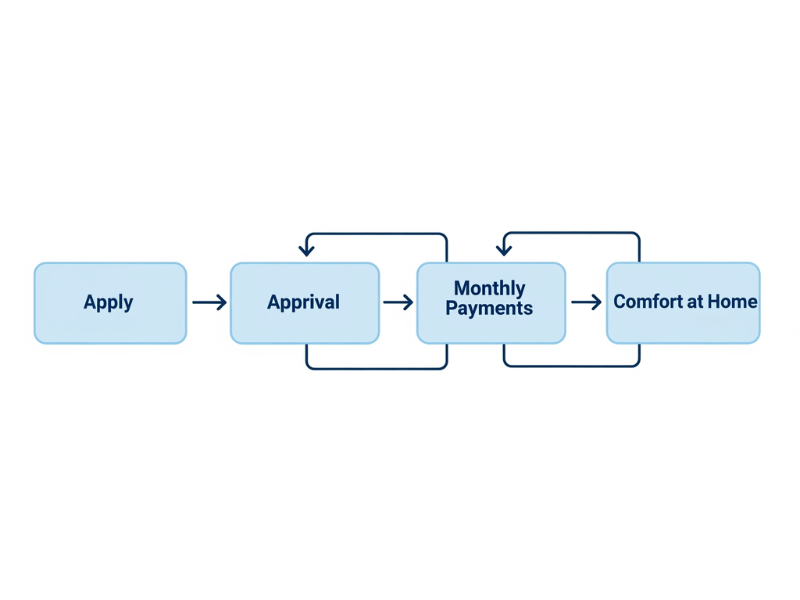

The first time I financed an HVAC system, I honestly felt like I was applying for a car loan. There’s paperwork, credit checks, and all those numbers they throw at you that can make your head spin. But once I broke it down step by step, it wasn’t nearly as scary as it looked.

Most applications start right at the contractor’s office or online through the lender. I remember sitting at my kitchen table filling out a quick form with my income, employment details, and the cost of the new system. Within minutes, I had a decision. It’s usually that fast, credit checks are automated these days. If you’re approved, you get an offer outlining the loan amount, interest rate, and repayment schedule. Some lenders will even cover the full installation cost, so you don’t pay a dime upfront.

This is where things can get tricky. When I had a credit score in the mid-700s, I was offered super low rates and even a 0% promo period. But when a friend of mine applied with a score in the low 600s, she was quoted a sky-high rate that made her payment almost double mine. Most lenders want to see a score above 650 to qualify for favorable terms, though some contractor financing plans accept lower scores with conditions. If your credit isn’t perfect, don’t stress, you still have options, but expect higher costs.

Interest rates for HVAC financing can range anywhere from 0% on promo deals to 20%+ if your credit isn’t great. Repayment terms are usually between 12 months and 10 years. For my system, I chose a 5-year loan at about 6% interest, which kept my payments manageable without dragging it out forever. The key is finding a balance between monthly affordability and not paying too much interest over time.

Let’s say your HVAC system costs $8,000. If you snag a 0% APR for 24 months, that’s about $333 per month until it’s paid off. If you go with a 5-year loan at 7% interest, your payment might drop to around $160 a month, but you’ll pay over $1,500 in interest by the end. That’s the trade-off, lower payments often mean more interest in the long run. I had to remind myself: monthly comfort now vs. total cost later.

At the end of the day, HVAC financing works like most other big-ticket loans. You apply, qualify based on credit and income, and then pay back the system over time. Once you understand the math, you’re in a better position to decide what actually works for your budget.

When I signed the dotted line for my HVAC loan, I felt both relief and hesitation. On one hand, my house was finally going to be livable again. On the other, I was adding another monthly bill to my stack. Financing definitely has its ups and downs, and knowing them ahead of time makes the decision less stressful.

The biggest pro? Affordability. Without financing, I’d probably still be sweating in my living room. Financing gave me the chance to replace my system immediately with payments I could actually handle. Another benefit is speed, you don’t have to wait months to save up the cash. Contractors love this too, because they can start the job right away. Plus, the terms are flexible. Some lenders give you short 12-month repayment windows, others spread it out over 10 years. You get to choose what fits your lifestyle.

Now for the not-so-fun part: interest. Unless you land a 0% APR promo and pay it off in time, you’re going to pay more than the sticker price. For my system, I ended up paying about $1,200 extra in interest over the life of the loan. That stung a little. The other downside is the commitment. Once you take out the loan, those monthly payments are locked in. Miss too many, and it can hit your credit hard. It’s like taking on a mini mortgage for your HVAC system.

I’ll be honest, financing isn’t always the right move. If you’ve got the cash in savings and won’t drain your emergency fund, paying outright saves you money in the long run. Financing also isn’t ideal if your credit score is really low. High interest rates could make the system cost thousands more than it should. I’ve also seen friends regret financing when they planned to move within a year. Investing in a system they wouldn’t even get to enjoy didn’t make much sense.

So, financing can be a lifesaver when you need an HVAC system now, but it’s not a one-size-fits-all solution. It comes down to your financial comfort zone, what feels manageable and smart for your situation.

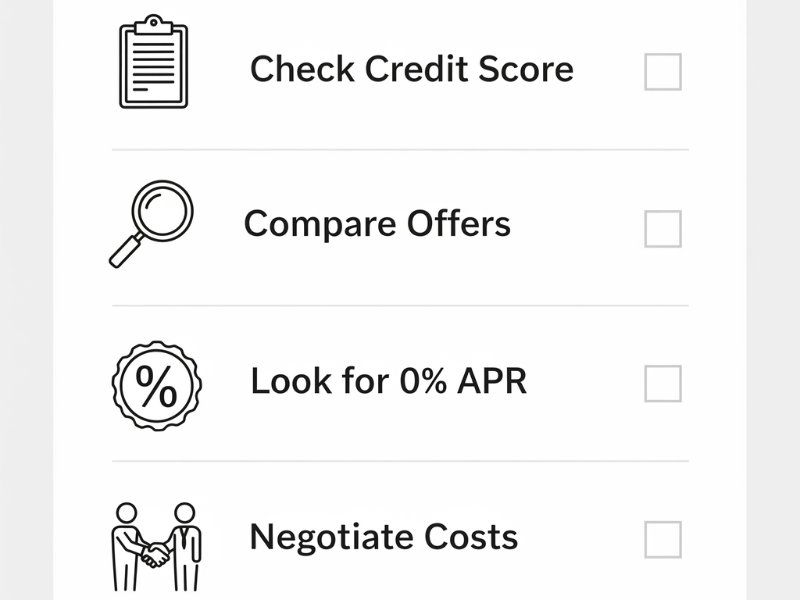

When I replaced my system, I realized financing wasn’t just about saying yes or no, it was about how to get the best deal possible. A little prep work saved me hundreds of dollars in the long run, and I wish I’d known these tips sooner.

Before filling out any application, I pulled my credit report. Turns out, my score was a bit higher than I thought, which gave me more leverage. If your score is solid, you can qualify for lower interest rates or even 0% promotional deals. If it’s not so great, don’t panic, sometimes paying down a credit card or fixing a small error on your report can bump your score enough to help you land a better offer.

When I first got a financing offer from my HVAC contractor, I almost said yes on the spot. Then I decided to shop around. I applied with my credit union and two online lenders just to compare. The rates and terms were wildly different, one offer would’ve cost me nearly double in interest over five years compared to another. Lesson learned: don’t settle for the first deal they throw at you.

This one’s gold if you can manage it. Some manufacturers and credit cards offer 0% APR for a limited time, usually 12–24 months. I snagged an 18-month 0% promo once and made it my mission to pay off the balance before the period ended. It wasn’t easy, but avoiding interest felt amazing. Just make sure you can realistically pay it off before the promo expires, or the backdated interest will hit hard.

Here’s something I didn’t realize at first: you can negotiate the system and installation price before you even get to the financing step. I asked my contractor for a breakdown and pointed out some competitor quotes I’d seen online. They actually dropped the price by almost $800. Lowering the principal means lower monthly payments and less interest overall. It’s worth speaking up, you’d be surprised how flexible contractors can be when they want your business.

At the end of the day, financing an HVAC system is about more than just getting approved. It’s about making smart choices before you sign. A little time spent checking credit, comparing offers, and negotiating can turn an “okay” financing deal into a great one.

I know financing makes sense for a lot of people, but it’s not the only path. When I replaced my first HVAC system, I almost jumped straight into a loan, but a friend reminded me to look at other ways to pay. Some of these alternatives can save you money and stress if they fit your situation.

If you’ve got the cash, this is hands-down the cheapest way to go. I paid for a smaller HVAC repair outright once, and it felt great knowing I wouldn’t be dealing with monthly bills. The trick is not to empty your entire emergency fund. If paying cash leaves you without a cushion for car repairs or medical bills, you might regret it later. But if you’ve been saving for home improvements anyway, this option saves you all that interest.

I didn’t know this the first time, but upgrading to an energy-efficient system can actually get you money back. Between federal tax credits and local rebates, you could save anywhere from a few hundred to over a thousand dollars. One of my neighbors installed a high-efficiency unit and got a $900 rebate from her utility company, plus a tax break at the end of the year. That’s free money you don’t want to miss out on.

Speaking of utilities, many companies have financing or rebate programs that are separate from contractors. Mine offered a low-interest loan specifically for energy-efficient HVAC systems. The process was surprisingly simple, and the interest rate was way lower than the bank’s personal loan option. It’s worth checking your utility provider’s website before making a final decision, you might find deals you didn’t expect.

Leasing an HVAC system is another alternative that doesn’t get talked about much. Instead of owning the unit, you pay a monthly fee to use it, kind of like renting. The upside is lower upfront costs and sometimes included maintenance. The downside is that you’ll never actually own the system, and those monthly payments can add up over time. I personally prefer financing because I like the idea of eventually owning the unit outright, but leasing could be handy if you’re on a super tight budget or planning to move soon.

Sometimes the smartest move is stepping back and asking: do I need financing, or is there another way to make this work? Exploring these alternatives first could save you thousands in interest, and that’s money you can put toward something way more fun than a furnace.

So, can you finance a new HVAC system? Absolutely, and for many homeowners, it’s the most practical way to handle a big expense without wrecking their budget. By exploring financing options, comparing terms, and taking advantage of rebates or promotions, you can upgrade your home’s comfort and energy efficiency while keeping payments manageable. Take the time to weigh the pros and cons, and don’t be afraid to negotiate. At the end of the day, the right financing plan can make your new HVAC system affordable, and that’s a win for both your wallet and your comfort.

Want to dive deeper into financial topics? Check out our other guides: