Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Managing your money at home doesn’t have to be complicated. Home finances involve managing your household’s income, expenses, savings, and investments. It’s your personal guide to financial stability and growth.

Think of home finances as the foundation of your financial house. Without proper management, even a high income can fall apart due to poor spending habits and lack of planning. Research shows that 64% of Americans live paycheck to paycheck – a situation you can avoid with proper financial management.

A solid home finance strategy includes these essential elements:

Your financial success starts with these basic building blocks. By mastering home finance management, you create a secure financial future, reduce stress, and build wealth steadily over time. The principles you’ll learn here will help you take control of your money and make informed decisions about your financial life.

In this article, we’ll explore the key components of effective home finance management and discover practical strategies you can implement today.

Budgeting is the foundation of managing your finances effectively. It’s like having a financial map that shows you where to spend and how to use your income wisely. With a well-thought-out budget, you can clearly see:

Having specific financial goals makes it easier to manage your money. Instead of just thinking about saving or paying off debt, you can break it down into concrete actions. Here are some examples of goals you might set:

Make sure each goal has specific numbers and deadlines attached to it. This way, you’ll know exactly what you’re working towards and when you want to achieve it.

To understand where your money goes each month, it’s important to categorize your expenses. This will help you identify areas where you can cut back or make adjustments. Here are the main categories to consider:

These are the costs that you cannot avoid or live without. They include:

These are the discretionary expenses that you have control over and can choose to reduce if needed. They include:

In addition to regular expenses, there are certain financial commitments that require your attention as well:

By breaking down your expenses into these categories and regularly tracking them, you’ll gain insights into your spending habits and be able to make informed decisions about optimizing your budget while still enjoying life along the way.

Managing your home finances requires a systematic approach that aligns with your financial goals and lifestyle. Let’s explore essential steps to create a solid financial foundation.

Your budgeting system should match your personality, financial habits, and life circumstances. Here are popular budgeting methods to consider:

Simple Budgeting Strategy for Beginners

If you’re just starting out or need a budget that allows some flexibility, try dividing your after-tax income into three basic categories:

To select the right budgeting system:

Remember: The best budgeting system is one you’ll consistently use. Start with your take-home pay after deductions and create a realistic plan that accommodates your financial goals while maintaining flexibility for life’s changes.

Tracking your spending habits is essential for successful budgeting. It provides you with accurate information to make informed financial decisions and understand your spending behavior.

By analyzing your spending data, you can find areas where you can cut costs. A thorough review often reveals surprising patterns – like those small daily purchases that add up significantly over time.

Creating a spending diary helps track emotional spending triggers. Note your mood and circumstances when making purchases – this insight helps develop healthier spending habits.

Regularly tracking your expenses can reveal opportunities to redirect money toward your financial goals without compromising your lifestyle. Small adjustments in your daily spending habits can lead to significant savings over time.

Automating your savings creates a hands-free approach to building wealth. You can set up automatic transfers from your checking account to designated savings accounts on each payday. This method removes the temptation to spend money earmarked for savings.

Your automated savings plan should align with the 50/30/20 rule, ensuring you’re dedicating at least 20% of your income to financial goals. Start with small, consistent amounts if you’re new to automated savings. You can increase these amounts gradually as your income grows or expenses decrease.

Schedule your automatic transfers for payday. This ensures your savings goals are met before you have a chance to spend the money on non-essential items.

Consider using a zero-based budget alongside your automation strategy to maximize savings potential. This approach assigns every dollar a specific purpose, including your automated savings transfers.

Life is constantly changing, and so should your budget. Major life events can have a big impact on your finances, and it’s important to make adjustments to your spending plan accordingly.

Your take-home pay may also fluctuate due to promotions, job losses, or additional sources of income. Whenever there is a change in your net income after deductions, it’s essential to recalculate your budget categories.

A zero-based budget or 50/30/20 rule framework can adapt to these changes. You may need to move funds between categories as necessary – for example, your “wants” allocation might temporarily decrease to accommodate new “needs” or savings goals.

The 50/30/20 rule provides a straightforward framework to allocate your after-tax income. Let’s break down each category:

The 50/30/20 rule serves as a flexible guideline – you might need to adjust these percentages based on your location, income level, and specific financial situation. Living in high-cost areas might require allocating more toward needs, while higher income levels might allow for increased savings percentages.

Smart financial planning requires a strategic approach to prioritizing your goals. Building a strong financial foundation starts with identifying and ranking your objectives based on their importance and urgency.

Your employer’s retirement plan match is essentially free money – a benefit you can’t afford to ignore. Here’s how to maximize this opportunity:

The power of compound interest makes early retirement contributions particularly valuable. A $5,000 annual investment starting at age 25 can grow to over $1 million by age 65, assuming an 8% average annual return.

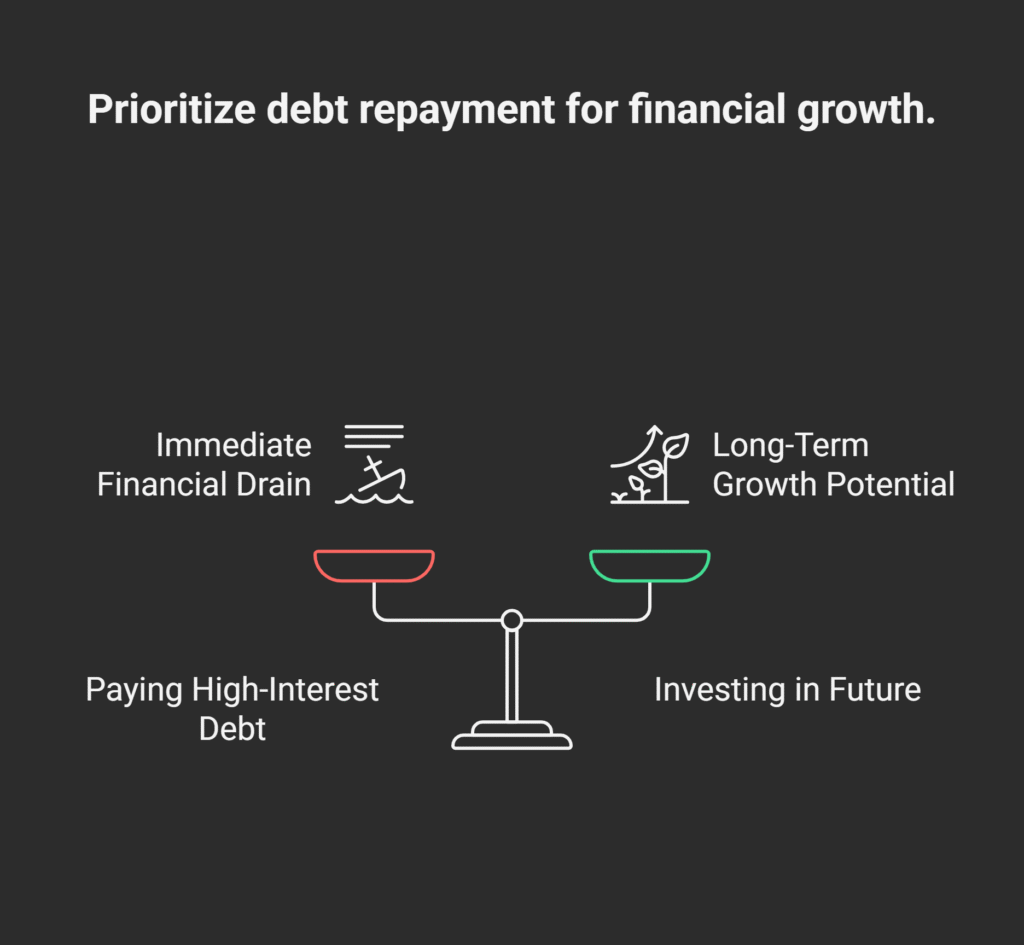

High-interest debt can drain your financial resources faster than you can build them. Credit card debt, with interest rates often exceeding 20%, creates a significant barrier to achieving your financial goals. Every dollar you pay in interest is a dollar that could have been invested in your future.

Here’s why prioritizing high-interest debt makes mathematical sense:

While focusing on high-interest debt, maintain a basic emergency fund:

If your employer offers retirement matching:

Track your progress using debt payoff calculators or apps to stay motivated and adjust your strategy as needed. Creating visual representations of your debt reduction can help maintain focus on your financial goals.

Balancing short-term needs with long-term goals creates a sustainable financial foundation. You can achieve this balance through:

The key lies in allocating resources proportionally. A practical approach is dividing your available funds after essential expenses:

This balanced distribution helps prevent financial strain while building lasting wealth. Regular monitoring and adjustments ensure your strategy remains aligned with changing life circumstances.

Managing your home finances doesn’t need to be complicated. The right combination of budgeting, tracking, and planning creates a solid foundation for your financial future. Your success in home finance management stems from:

Remember: financial stability is a journey, not a destination. Start with small steps, celebrate your progress, and adjust your strategy as needed. The habits you build today shape your financial future tomorrow.

Take action now – pick one area of your home finances to focus on this week. Whether it’s tracking your spending, setting up automatic savings, or reviewing your budget, each step brings you closer to your financial goals. Your future self will thank you for the financial decisions you make today.

Ready to take control of your home finances? Start implementing these strategies today.

Home finance management involves effectively managing your money at home, including budgeting, setting financial goals, and tracking expenses. It’s crucial for achieving financial stability and securing a comfortable future.

Choosing a budgeting system depends on your lifestyle and preferences. Popular methods include the 50/30/20 rule, zero-based budgeting, and the envelope system. Evaluate each to find one that helps you balance needs, wants, and savings effectively.

Regularly tracking your spending helps you stay within your budget, identify unnecessary expenses, and implement cost-cutting strategies without compromising quality of life. It ensures better control over your take-home pay after deductions.

Automating savings ensures consistent contributions towards important financial goals like building an emergency fund or saving for retirement. This approach leverages after-tax income effectively and reduces the temptation to spend what you intend to save.

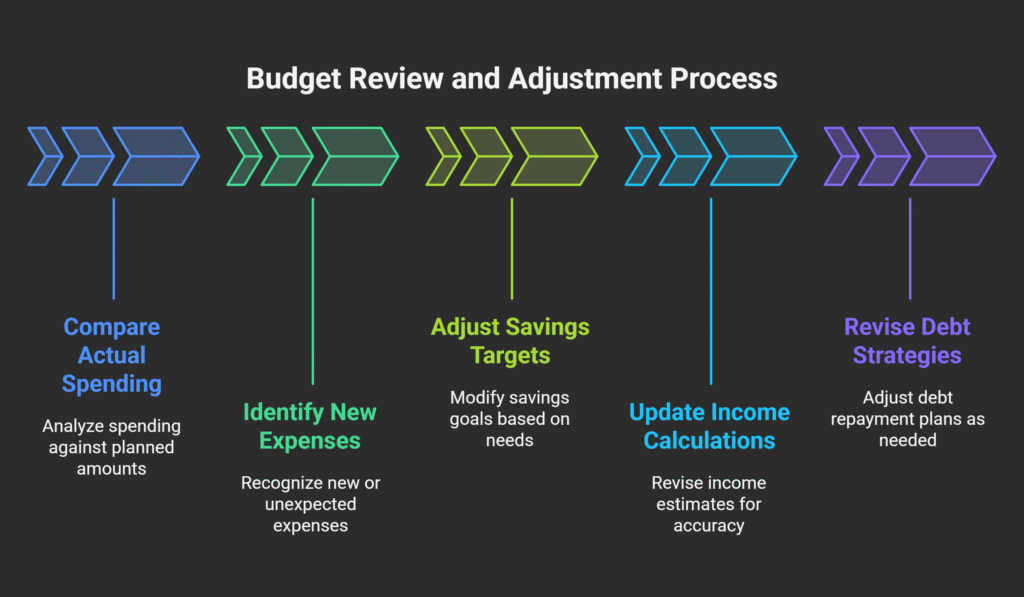

You should review and adjust your budget periodically, especially after significant life changes such as having a baby or buying a house. Income fluctuations and new priorities may require modifying your budget to maintain financial stability.

Key priorities include building an emergency fund as a safety net against unexpected expenses, taking full advantage of employer retirement plan matches early on, and paying off high-interest debt before focusing on other financial goals like saving for retirement.