Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Did you know that nearly 57% of U.S. workers rely on employer-provided life insurance, but most policies only cover one to two times your annual salary? That’s rarely enough for long-term family protection! This is where supplemental life insurance comes in.

In this article, we’ll break down what supplemental life insurance actually is, when you might need it, and how to decide if it’s a smart move for your financial plan. We’ll look at real-world examples, compare costs, and uncover the truth about whether this add-on coverage is worth it, or just another expense.

At its core, supplemental life insurance is extra coverage that you can add on top of your basic life insurance policy, usually through your employer. Most companies automatically provide some form of basic life insurance as part of their benefits package, but it typically only equals one to two times your annual salary. That sounds helpful at first, but if you add up your mortgage, debts, childcare, and day-to-day family expenses, it’s rarely enough.

Supplemental coverage is designed to fill that gap. Unlike employer-paid basic coverage, supplemental life insurance is usually voluntary, you pay for it yourself through payroll deductions. Think of it as a way to boost your financial safety net if the standard policy doesn’t quite cut it.

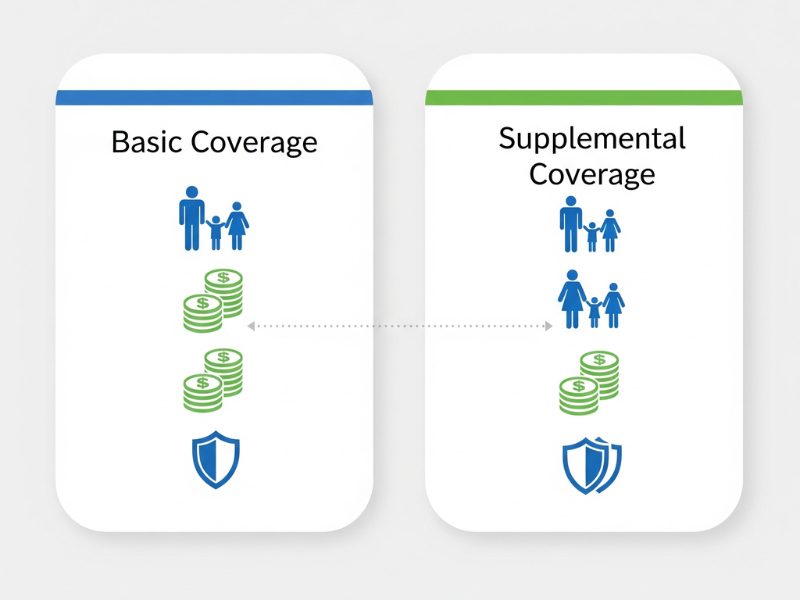

The main difference between basic and supplemental life insurance comes down to cost and flexibility. Basic coverage is free or heavily subsidized by your employer, while supplemental coverage is optional, and the premiums come directly from your paycheck.

With supplemental coverage, you can often choose higher coverage amounts, add protection for a spouse or children, and sometimes even select between term or whole life options. In other words, it gives you more control over how much protection your family really gets.

Imagine your employer gives you $50,000 of basic life insurance at no cost. That might sound fine, but if your family depends on your income, it wouldn’t last long. By enrolling in supplemental life insurance through your workplace, you could increase your coverage to $250,000 or more, depending on your company’s offerings.

That extra $200,000 could make a huge difference for your loved ones, helping them cover living expenses, mortgage payments, or even college tuition if something happened to you.

Most people get supplemental life insurance through their employer during open enrollment. You’ll usually see it listed as a voluntary benefit alongside health insurance and disability coverage. Signing up is simple, usually just a few clicks in your benefits portal. Premiums are deducted straight from your paycheck, so you don’t have to worry about missing a payment.

Sometimes you’ll be automatically approved up to a certain coverage amount without needing to answer medical questions. This is called “guaranteed issue.” For higher amounts, you might have to complete a health questionnaire or take a basic medical exam.

The cost of supplemental life insurance depends on a few factors: your age, the amount of coverage you choose, and whether you add a spouse or children to the policy. Since it’s often offered at group rates, premiums can be lower than what you’d pay for an individual policy, at least when you’re younger.

But here’s the catch: those premiums can increase as you get older. What feels affordable at 30 may look pretty steep at 50. It’s worth checking if your plan locks in your rate or if it’s age-banded, meaning the price rises every five or ten years.

One of the biggest advantages of supplemental life insurance is flexibility. Most employers give you several choices for coverage levels and add-ons:

Let’s say you earn $60,000 a year and your company provides a basic $60,000 life insurance policy. During open enrollment, you decide to add $240,000 in supplemental coverage, bringing your total coverage to $300,000. The premiums are automatically deducted from your paycheck each month, making it hassle-free.

If you were to pass away, your family would receive the full $300,000 payout—basic plus supplemental. That’s a much stronger financial cushion than the $60,000 alone.

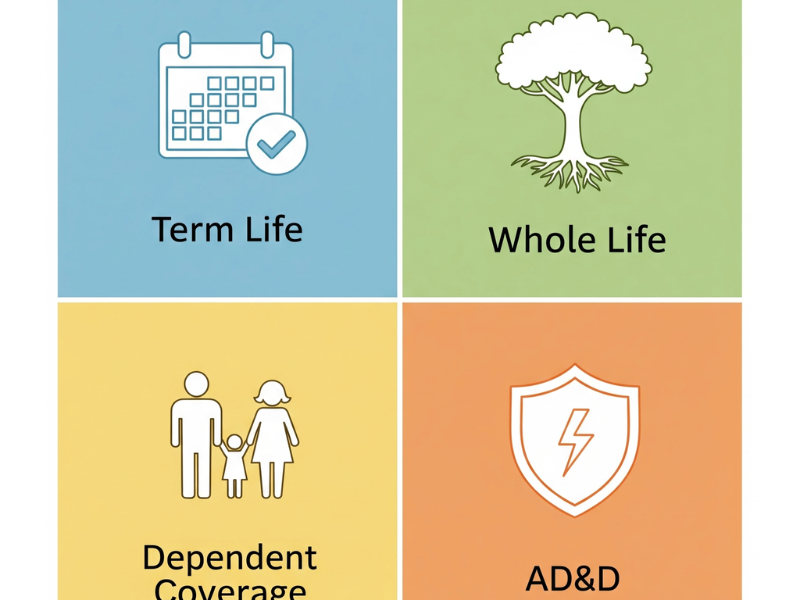

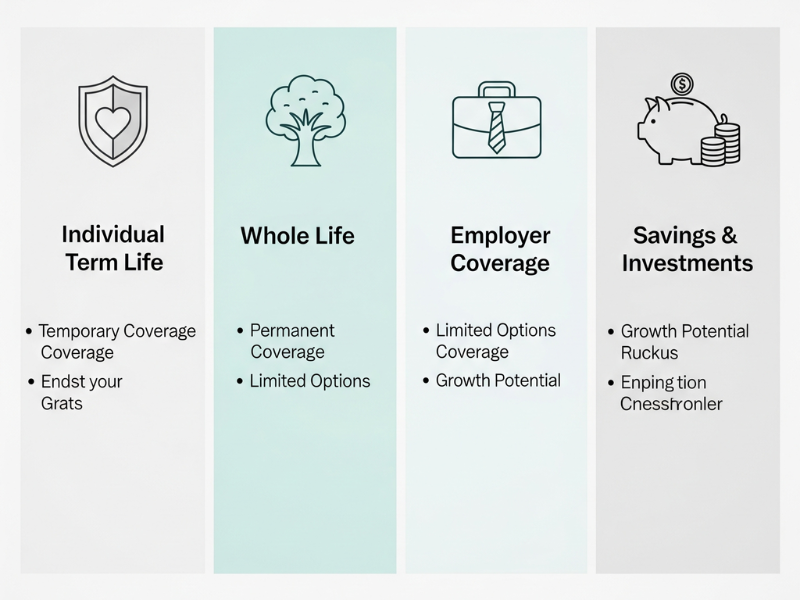

This is the most common type of supplemental coverage. Term life insurance provides protection for a set period, usually 10, 20, or 30 years. It doesn’t build cash value, but it’s affordable and gives a straightforward payout if something happens to you during the term.

Many employers offer supplemental term life in increments, like $50,000 or $100,000, so you can tailor it to your family’s needs. It’s especially useful if your goal is to cover debts, mortgage, or college expenses.

Some companies offer supplemental whole life insurance, though it’s less common. Unlike term life, whole life coverage lasts your entire lifetime and accumulates cash value. The premiums are higher, but it can be a more permanent financial tool if you want lifelong protection for your family.

Whole life policies through your employer are usually simpler than buying one individually. They might have fewer bells and whistles, but they get the job done without complicated underwriting.

Dependent coverage is another option under supplemental life insurance. This allows you to insure your spouse or children for a smaller, fixed amount.

This type of coverage is optional but can be valuable if you want to make sure your loved ones are protected without buying separate policies.

Some employers offer AD&D as part of supplemental life insurance. This policy pays an additional benefit if you die or suffer severe injuries in an accident, like losing a limb or eyesight.

It’s not a replacement for regular life insurance, but it can be a helpful add-on, especially for those with physically demanding jobs or adventurous lifestyles.

Understanding the different types of supplemental life insurance helps you make an informed choice. Term life is affordable and practical, whole life adds permanence, dependent coverage protects your family, and AD&D adds extra safety in risky situations.

When choosing coverage, think about what your family would need financially if something unexpected happened, and pick the combination that covers your most pressing risks.

One of the biggest perks of supplemental life insurance is how easy it is to sign up. Most employers allow you to enroll during open enrollment or when you first join the company. For coverage amounts within guaranteed limits, you often don’t need a medical exam, just a few questions about your health. That convenience makes it accessible for people who might otherwise struggle to get life insurance.

Because supplemental life insurance is offered through your employer, you usually get group rates, which can be significantly cheaper than buying an individual policy on your own. The cost is often deducted directly from your paycheck, making it feel less like a bill and more like an automatic financial safety net.

The main advantage, of course, is the peace of mind that comes with knowing your family would be protected if something unexpected happened. Supplemental coverage can help pay off debts, cover mortgage or rent, fund children’s education, or simply provide a financial cushion to maintain your family’s lifestyle.

Many plans let you tailor your coverage to your needs. You can often select higher amounts, add dependent coverage for your spouse or kids, or choose term or whole life options. Some employers even offer accidental death and dismemberment coverage as an optional add-on. This flexibility ensures you’re not paying for coverage you don’t need while still providing adequate protection.

Since premiums are automatically deducted from your paycheck, it’s easy to stay current without having to remember monthly payments. This also reduces the risk of accidentally letting your policy lapse, which can happen with individual plans if payments are missed.

Finally, having supplemental life insurance through work gives a layer of security without adding stress to your life. You know you have a safety net in place, and it can complement any personal life insurance policies you already own.

I remember a friend of mine who initially ignored supplemental life insurance because she thought her basic coverage was enough. When she got married and bought a house, she realized the basic policy wouldn’t cover their mortgage if anything happened to her. Signing up for supplemental coverage added that extra financial cushion without complicated paperwork or high premiums.

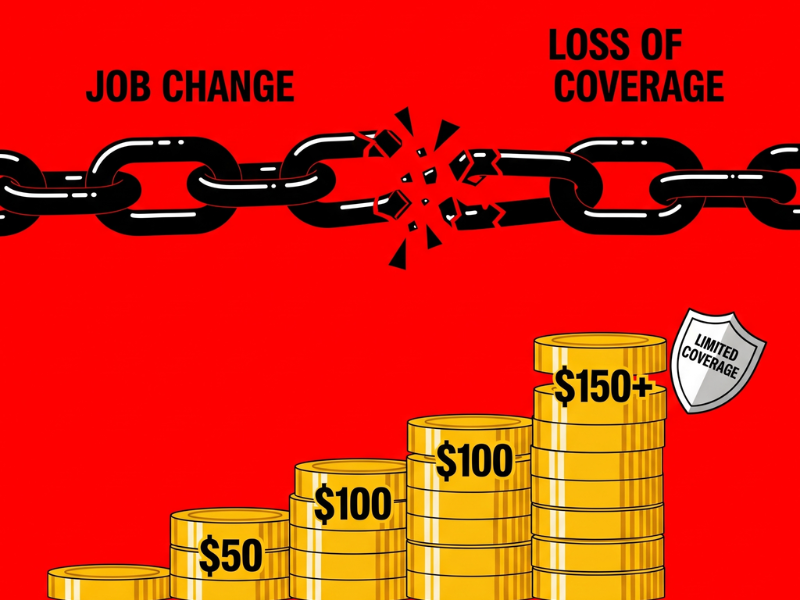

One of the biggest drawbacks of supplemental life insurance is that it’s usually linked to your employer. If you leave your job or get laid off, you may lose the coverage. Some plans allow you to convert your policy to an individual plan, but the premiums can be much higher once you’re no longer part of the group.

Supplemental life insurance often has caps on how much coverage you can buy. If you have significant debts, a large mortgage, or multiple dependents, the maximum offered by your employer might not be enough. In those cases, you might still need a separate individual life insurance policy to fully protect your family.

Even though group rates are affordable when you’re younger, premiums often increase as you get older. Some plans are age-banded, meaning your cost jumps at certain age milestones, which can make long-term planning tricky. It’s important to check your employer’s policy details so you’re not caught off guard.

While some employers allow policy conversion, many do not. That means your coverage might vanish if you change jobs, which can leave you underinsured unless you take action to secure a new policy.

Supplemental life insurance is designed to be simple, which is great for convenience but can be a downside if you want more control. You often can’t pick all the features of your policy like you could with an individual life insurance plan. For example, adding riders or cash value options may be restricted or unavailable.

I remember a colleague who had relied entirely on her employer’s supplemental coverage. When she changed jobs, she didn’t realize the policy wouldn’t follow her, and she had a brief gap in coverage. Thankfully, she quickly purchased an individual policy, but it was a costly lesson in understanding the limitations of employer-linked insurance.

Supplemental life insurance can be a convenient and affordable way to add coverage, but it’s not a one-size-fits-all solution. You need to weigh the benefits against the risks, especially if job changes or long-term financial planning are on the horizon.

One of the biggest differences between supplemental and individual life insurance is flexibility. Supplemental coverage through your employer is convenient and affordable, but it often comes with limitations. Individual life insurance policies, on the other hand, give you more control over the coverage amount, policy type, and added features like riders or cash value accumulation.

With an individual policy, you can customize your plan to fit your family’s specific needs rather than sticking to the increments and options your employer offers. This can be particularly important if you have a mortgage, multiple dependents, or unique financial obligations.

Supplemental life insurance usually comes with a maximum coverage limit set by your employer, which may not fully replace your income or cover large expenses. Individual policies typically allow for higher coverage amounts, making them better suited for long-term financial planning.

At first glance, supplemental life insurance seems cheaper because premiums are deducted from your paycheck and may be subsidized by your employer. But remember: as you age, premiums for group coverage can increase, and portability isn’t guaranteed.

Individual life insurance may cost more upfront, but it can lock in rates for decades and stay with you even if you change jobs. Over time, this stability can actually save money and prevent coverage gaps.

Choosing between supplemental and individual life insurance depends on your situation:

I knew someone who relied solely on supplemental life insurance through work. When they switched employers, they realized the coverage didn’t transfer, and premiums for an individual policy were higher than expected. If they had purchased an individual policy earlier, they would have had continuous coverage and locked-in rates, avoiding stress and extra costs.

Supplemental life insurance is a convenient safety net, but it shouldn’t be your only option if you need comprehensive, long-term protection. Combining supplemental coverage with an individual policy often provides the best of both worlds, affordable immediate coverage and flexible, permanent protection for the future.

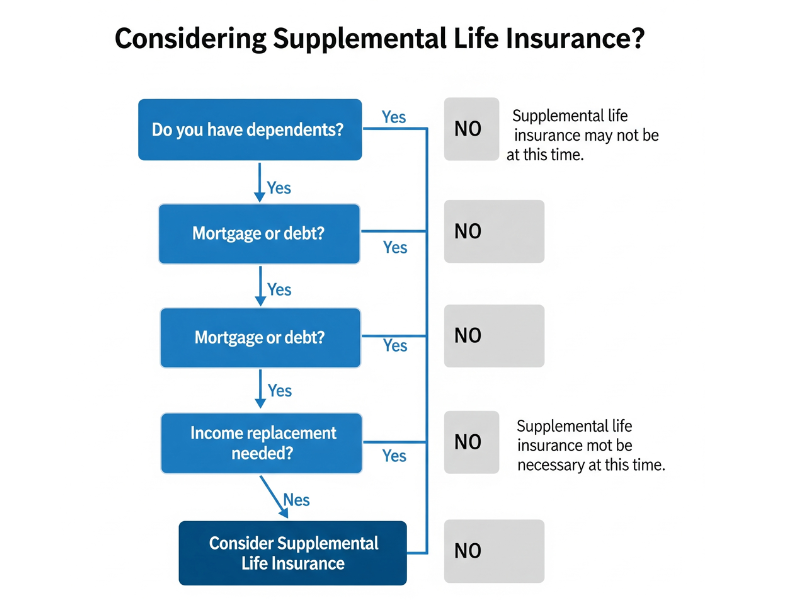

Before signing up for supplemental life insurance, it’s important to evaluate your actual needs. Ask yourself questions like:

Answering these questions can help you determine whether supplemental coverage is necessary or if your existing policies are enough.

Several factors can influence whether supplemental life insurance is right for you:

Supplemental life insurance is often a smart choice if:

In some cases, individual life insurance policies may be more suitable:

I had a coworker who initially passed on supplemental life insurance, thinking her basic coverage was sufficient. When she had her first child, she realized her coverage wouldn’t fully protect her family if something happened. Signing up for supplemental insurance was quick, affordable, and gave her peace of mind knowing her family had an extra financial cushion.

Deciding whether to get supplemental life insurance comes down to your personal circumstances. Assess your family’s financial needs, consider your debts and income replacement goals, and weigh the convenience of employer-provided coverage against the flexibility of an individual policy.

A common guideline is to aim for 10–12 times your annual income in total life insurance coverage, including both your employer-provided basic coverage and any supplemental policy. This ensures that if something happens to you, your family has enough to cover living expenses, debts, and future goals like college tuition or retirement.

To determine the right amount of supplemental coverage, consider:

You can use online life insurance calculators to get a rough estimate of how much coverage your family might need, then subtract the amount of basic life insurance provided by your employer. The remainder is the supplemental coverage to consider.

Remember that premiums often rise with age, so it can be wise to enroll earlier when rates are lower. This approach can make higher coverage amounts more affordable over the long term.

Since supplemental coverage is typically tied to your employer, think about your career path. If you plan to change jobs, you may need to consider an individual life insurance policy to maintain coverage continuity.

I know someone who initially bought minimal supplemental coverage. As their family grew, they realized the initial amount wasn’t enough to cover the mortgage and future college expenses. They adjusted their supplemental coverage incrementally, which kept premiums manageable while providing the right level of protection.

There’s no one-size-fits-all answer, but calculating your debts, income needs, and future expenses gives a clear picture of how much supplemental life insurance makes sense. Combine this with your basic employer coverage to ensure your family is fully protected.

If supplemental life insurance through your employer doesn’t meet your needs, an individual term or whole life insurance policy might be a better fit. Term life policies are generally more affordable and provide coverage for a specific period, like 10, 20, or 30 years. Whole life policies, while more expensive, offer permanent coverage and can accumulate cash value over time.

Individual policies give you more control and flexibility than employer-based supplemental coverage. You choose the coverage amount, term length, and any optional riders to customize the policy to your family’s unique needs.

Some people use their employer-provided life insurance as a baseline and then purchase an individual policy to fill in the gaps. This approach ensures you have coverage right away without committing to a large individual policy, which can be more costly upfront.

It’s a practical way to get immediate protection while planning for long-term security. You can adjust your individual policy later as your financial situation changes.

Life insurance isn’t the only way to protect your family. Consider other strategies alongside or instead of supplemental coverage:

These options can complement life insurance or, in some cases, reduce the amount of supplemental coverage you need.

I had a friend who relied solely on her employer’s supplemental coverage. She later realized her family’s financial needs would have been better met with a combination of her basic policy, an individual term life policy, and a small emergency fund. This mix gave her both flexibility and long-term security without depending entirely on one type of coverage.

Alternatives to supplemental life insurance allow you to tailor coverage to your exact needs, provide portability beyond your job, and potentially offer better long-term financial planning. Don’t overlook these options when deciding how to protect your family.

Supplemental life insurance is an affordable and convenient way to boost your employer-provided coverage. It fills the gap between basic life insurance and the financial protection your family truly needs. If you have dependents, debts, or long-term financial goals, it’s worth seriously considering.

While supplemental coverage is easy to enroll in, often cheaper than individual policies, and provides payroll-deducted convenience, it has some limitations. Coverage is usually tied to your job, may have maximum limits, and premiums can increase with age. Understanding these factors helps you make informed decisions and avoid coverage gaps.

Deciding how much supplemental coverage to get requires assessing your debts, income replacement needs, and future expenses. Use online calculators or work with a financial advisor if needed. Remember, the goal is to ensure your loved ones are protected without overpaying for unnecessary coverage.

Employer-provided supplemental life insurance isn’t your only option. Individual term or whole life policies, combined with an emergency fund or disability coverage, can give you flexibility, portability, and long-term security. Often, the best approach is a mix of employer coverage and individual policies tailored to your situation.

Don’t wait until it’s too late. Review your current life insurance coverage, calculate your family’s financial needs, and explore supplemental options during open enrollment. Even a small increase in coverage can provide significant peace of mind.

Life insurance can be confusing, but understanding supplemental options is empowering. With the right coverage, you can protect your family, secure your financial future, and avoid the stress of leaving loved ones underinsured.

Supplemental life insurance isn’t just another benefit, it’s a safety net that can protect the people who matter most. It’s the quiet assurance that, if life throws the unexpected your way, your family won’t have to face it alone.

Sure, it has limits and nuances, but understanding how it works puts you in control. By evaluating your debts, income replacement needs, and long-term goals, you can craft a coverage plan that truly fits your life. Whether you stick with supplemental coverage, add an individual policy, or combine both, the goal is the same: protection, security, and peace of mind.

The real takeaway? Don’t leave it to chance. Open enrollment is the perfect opportunity to review your coverage, calculate your family’s needs, and make thoughtful choices. Even a modest increase in supplemental life insurance can transform your family’s financial future.

In the end, this isn’t just about insurance, it’s about choosing confidence and security for the ones you love. Take the step today and give yourself the gift of knowing you’ve got it covered.

Want to dive deeper into financial topics? Check out our other guides:

Supplemental life insurance is additional coverage you can purchase on top of your employer-provided basic life insurance. It helps fill gaps so your family has enough financial protection in case something happens to you.

You usually enroll through your employer during open enrollment. Premiums are deducted from your paycheck, and coverage can include yourself, your spouse, or your children. Some policies may require a health questionnaire or medical exam for higher coverage amounts.

It’s ideal for people who have dependents, outstanding debts, a mortgage, or long-term financial obligations. If your basic employer coverage isn’t enough to meet your family’s needs, supplemental life insurance can provide extra financial security.

The most common types are term life insurance (coverage for a set period) and, less commonly, whole life insurance (permanent coverage with cash value). Many plans also offer dependent coverage for spouses and children and accidental death and dismemberment (AD&D) options.

Costs vary based on age, coverage amount, and whether you include dependents. Group rates through your employer are typically more affordable than individual policies, and premiums are usually deducted directly from your paycheck.

Not always. Most employer-provided supplemental policies are tied to your job. Some plans allow you to convert the policy to an individual plan, but premiums are usually higher.

A common guideline is to aim for 10–12 times your annual income in total coverage, combining both your basic and supplemental policies. Consider your debts, income replacement needs, and future expenses when deciding how much to purchase.

Many employer plans offer optional dependent coverage. Spouse coverage helps protect your partner, and child coverage usually provides a smaller payout for funeral or early financial needs.

Limitations include coverage caps, reliance on your employment, increasing premiums with age, and less customization compared to individual policies. It’s important to review these factors before enrolling.

Yes! Many people use supplemental coverage through work as a baseline and add an individual policy for extra protection or higher coverage. This combination provides both convenience and long-term flexibility.